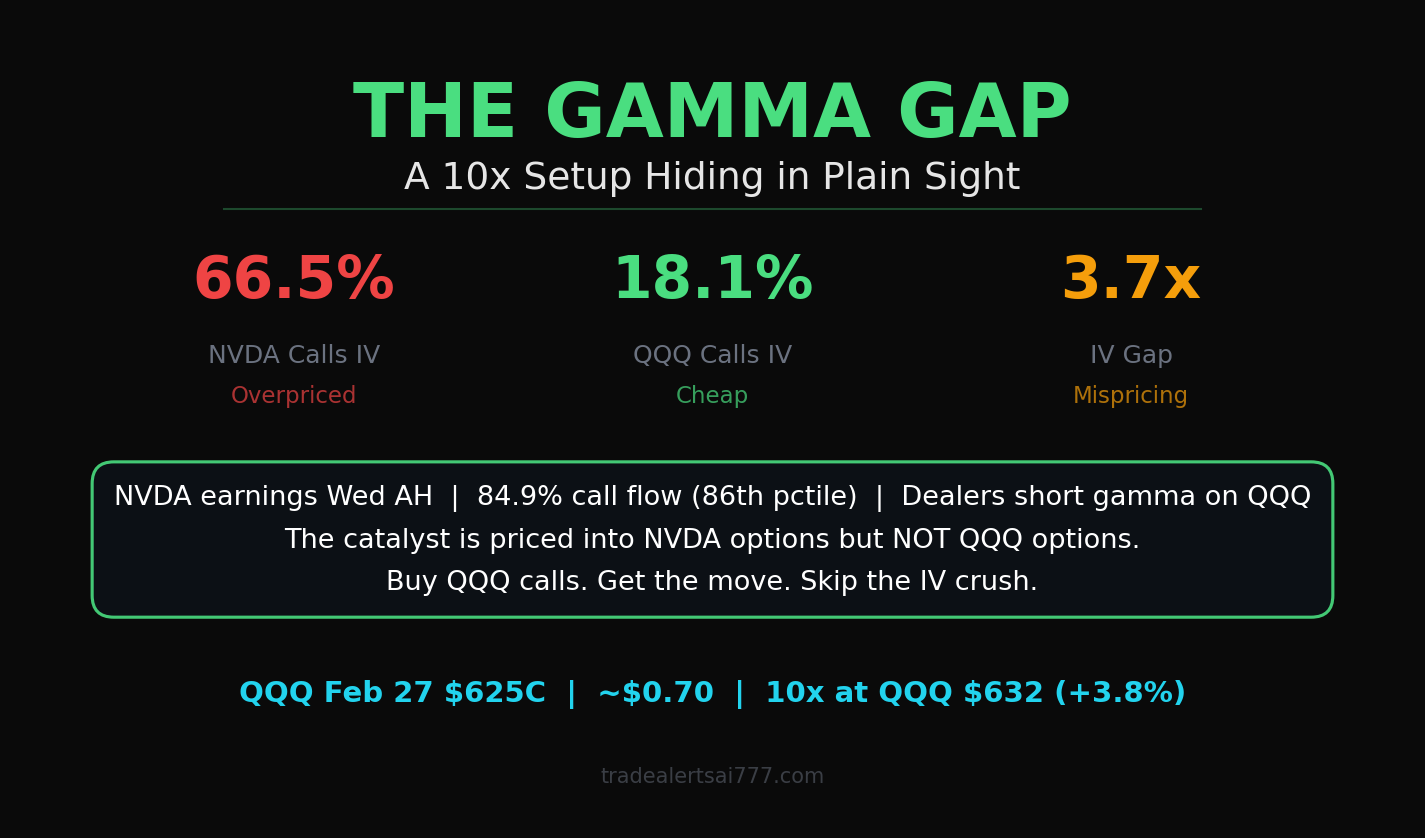

The Setup

NVIDIA reports earnings Wednesday after hours. The flow is 84.9% calls — sitting at the 86th percentile of the last 30 days. Dark pool has accumulated $993M notional. Every data point we track says the smart money is positioned for a beat.

So naturally, every retail trader on earth is loading up on NVDA call options.

And that's exactly the problem.

The IV Trap

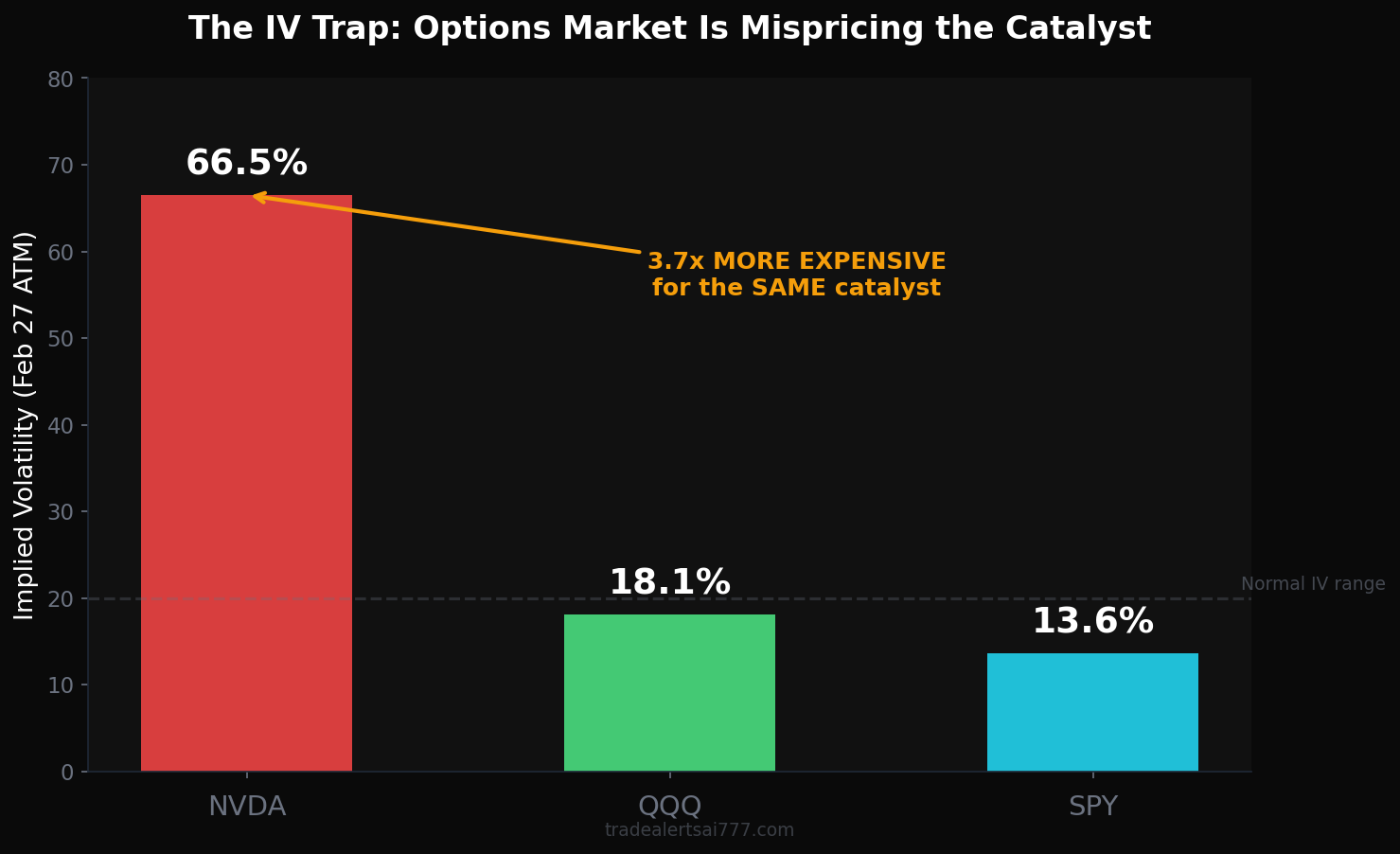

When everyone piles into the same trade, the options market adjusts. NVDA weekly call implied volatility has been jacked up to 66.5%. That's 3.7x more expensive than QQQ calls at the same expiry.

Here's what that means in practice: even if NVDA beats earnings and rallies 8%, IV crush destroys roughly 40% of your call premium overnight. You could be right on direction and still lose money.

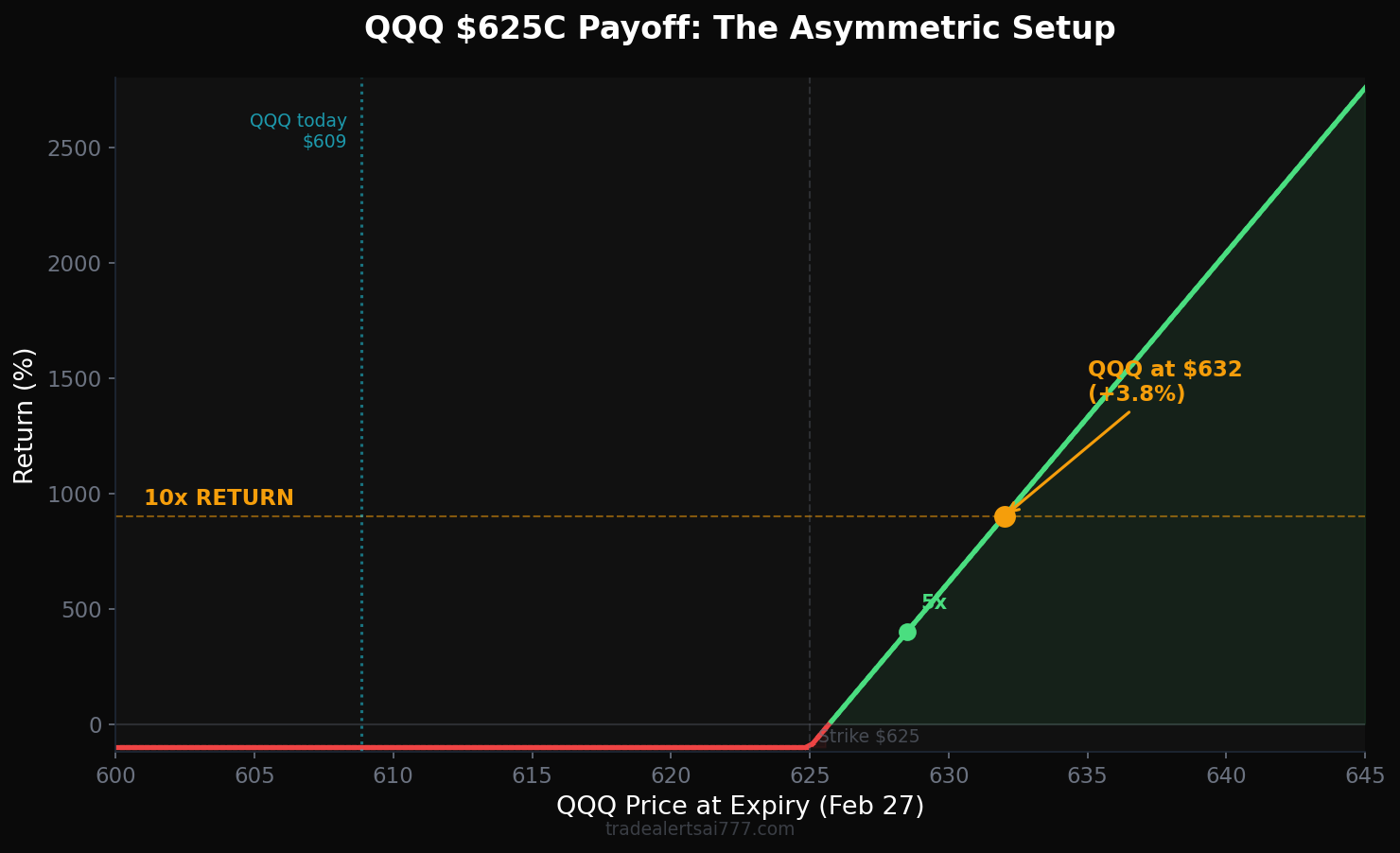

The NVDA $195 call costs $3.57. For a 10x return, you'd need NVDA at $231 — a +22% move in one week. That's not a trade. That's a prayer.

The Gamma Gap

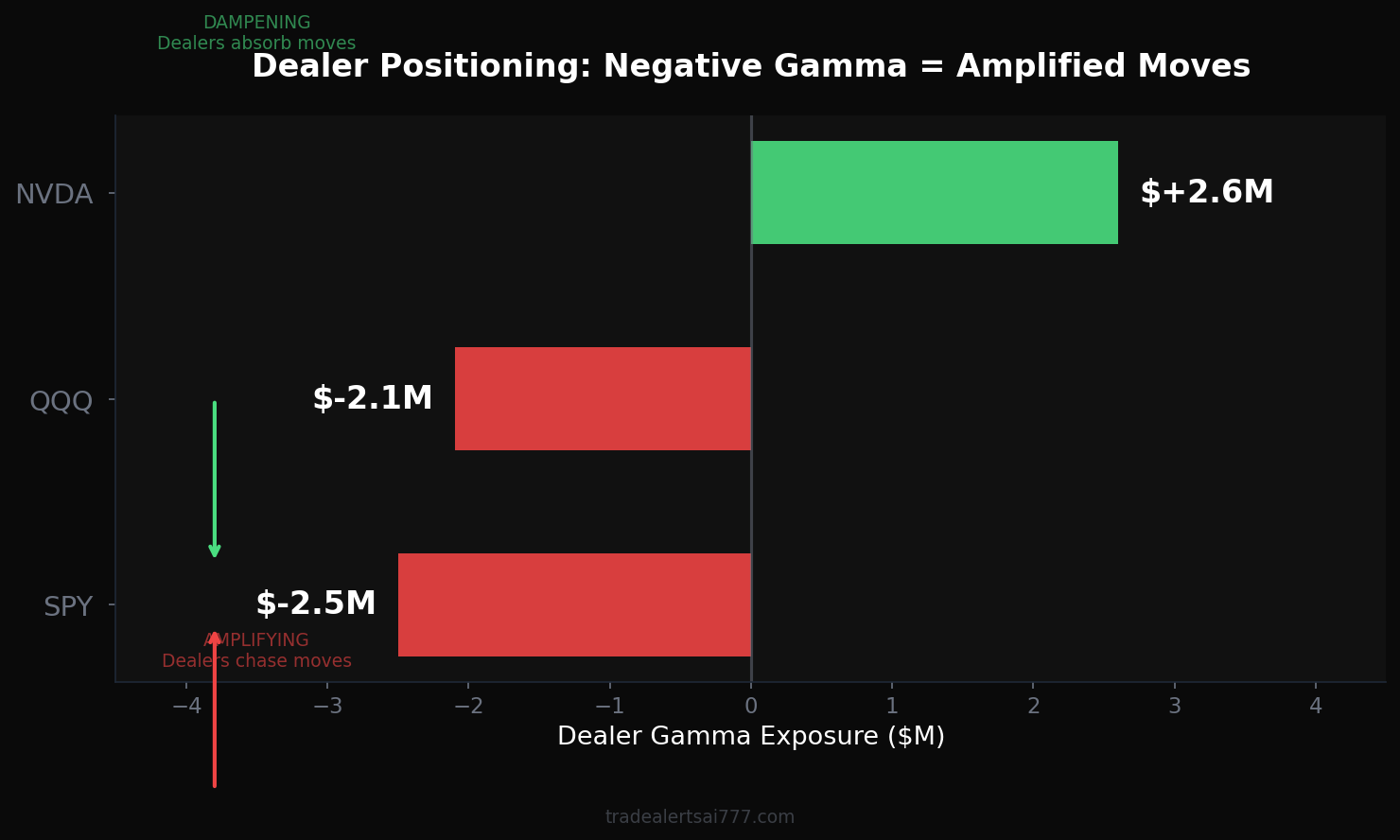

Now here's where it gets interesting. While everyone is staring at NVDA options, the index-level dealer positioning is telling a completely different story.

Dealers are sitting at -$2.1M gamma on QQQ and -$2.5M on SPY. Negative gamma means when the market moves, dealers have to chase it — buying more as it goes up, selling more as it goes down. They amplify the move rather than dampen it.

Meanwhile, NVDA has +$2.6M positive gamma. Dealers are long gamma on NVDA, which means they absorb moves. Paradoxically, the index could move more explosively than the underlying catalyst stock.

This is the gamma gap: the catalyst is priced into NVDA options, but the amplification mechanism lives in QQQ.

The Flow Tells the Story

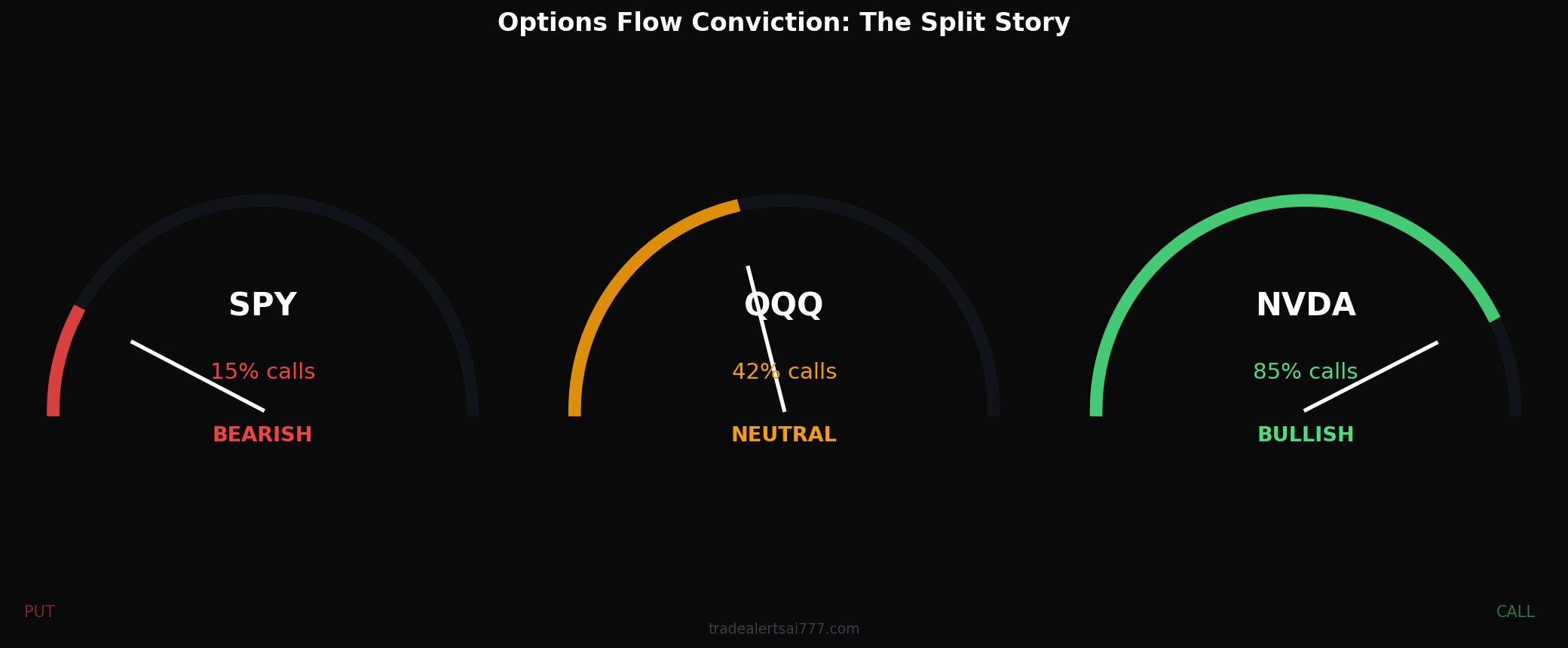

Look at the split:

- NVDA: 85% call flow, 86th percentile, screaming bullish. This is the catalyst.

- QQQ: 42% calls, neutral. The market isn't positioned for a QQQ move. That's the opportunity.

- SPY: 15% calls, deeply bearish. Index-level hedging is heavy. This unwinds violently on a risk-on move.

When NVDA beats (and the flow says it will), that single stock contributes ~0.9% to QQQ directly. Add tech sympathy from AMD, AVGO, MSFT rallying. Add the negative gamma cascade where dealers are forced to buy. Total QQQ move potential: +3-4% in two trading days.

The Trade

Instrument: QQQ calls (NOT NVDA)

Thesis: NVDA beat + negative dealer gamma cascade = QQQ rip

Edge: IV mispricing — the catalyst is priced into NVDA (66% IV) but not QQQ (18% IV)

Entry Timing

Monday open for Mar 6 calls — QQQ is down 0.8% after-hours, so you're buying the dip. More time means theta isn't punishing.

Wednesday ~3:50 PM for Feb 27 calls — let theta destroy the premium first, then buy right before the catalyst. Maximum leverage at minimum price.

The Payoff

Why Not NVDA Calls?

It's the most intuitive trade in the world: NVDA is going to beat, so buy NVDA calls. But intuitive trades rarely 10x, because everyone already thought of them.

The NVDA $200C (5.6% OTM) costs $1.98. For 10x, you need NVDA at $220 — a +16% move in one week. IV crush alone destroys 40% of the premium the morning after earnings. You're fighting the house.

QQQ calls give you 9% NVDA exposure, tech sympathy, AND the negative gamma amplifier — all at 18% IV instead of 66%. Same catalyst. 3.7x cheaper. No IV crush.

The options market priced the catalyst into the wrong instrument. That's the edge.

The Risk

This is a lottery ticket, not a retirement plan. The risks are real:

- NVDA misses or guides weak: Negative gamma amplifies the downside. QQQ craters. Both positions expire worthless.

- Beat but "sell the news": NVDA rallies 5% post-earnings but the index is flat. QQQ calls don't move enough.

- Macro event: Geopolitical shock, Fed surprise, or tariff headline overrides the earnings catalyst.

- Theta decay: Feb 27 calls lose value every hour they don't move. They can go to zero fast.

Size accordingly. This is money you can afford to lose entirely. The asymmetry is the point — risk small, win big if right.

The Gamma Gap, summarized in one line:

The catalyst is priced into NVDA options, but the amplification lives in QQQ options. Buy the amplifier, not the catalyst.

No other service gives you the full picture like this — the raw data, the detailed reasoning, the exact contracts, and when to pull the trigger. Not vague "I'm bullish" tweets. Not paywalled Discord alerts with no explanation. We show you the IV mispricing, the dealer positioning, the flow conviction, and walk you through the trade construction step by step.

This kind of analysis is just one of the bonus deep-dives that come with your founding membership. On top of it, you get:

- Real-time options flow & dark pool tracking

- AI-powered pattern detection

- Dealer Signal Dashboard — 103 tickers, 4x daily (nothing like it exists)

- GEX Maps with directional gamma

- Daily ML-scored top plays

$39.99/month — founding member price, locked in forever. Join now →